Description of the approach to ensure the quality of the published information

The MSG must ensure the quality of reporting on payments made by companies to government agencies as well as the corresponding government revenues. This is a key requirement of the EITI standard. In the first two D-EITI reports, the MSG relied on mutual disclosure of payment flows for quality assurance. This so-called EITI standard procedure provides for an individual comparison of the reported payments of companies with the corresponding revenues of the government agencies by an Independent Administrator. There were no or no notable differences between payments made by companies and payments received from government agencies.

From a systematic point of view, the standard payment reconciliation procedure is a case-by-case examination of the payment flows reported by the participating companies. There is no recording and assessment of the processes and controls associated with the payment flows.

Since the 2018 reporting period, Germany has been developing and implementing an alternative method for quality assurance of reported payment flows to government agencies. For this eighth German EITI report, the alternative method will continue to be used by the MSG and the Independent Administrator.

The alternative method replaces payment reconciliation with a two-step system-based approach. In its first step, information about the relevant processes and controls as well as the control environment is collected and analysed. The focus is essentially on the government payment recipients, for example the collection processes of the government agencies, the existing monitoring bodies or the general legal framework conditions in the government agencies. The aim of the analysis is to enable the MSG to make an informed assessment of whether there are risks of incorrect processing of extraction-related payments to government agencies during the reporting period.

Depending on the result of the risk assessment, different steps are derived: from a plausibility check based on key figures or further analytical considerations in the case of missing risk indications to detailed analyses/checks in the case of risk indications.

The concept of the system-based approach developed under the alternative quality assurance process is considered appropriate to meet the requirements of the EITI standard on the reliable disclosure of payments from the extractive industries. In the meantime, the alternative has been included as an EITI standard procedure.

The investigative actions of the company reports carried out by the Independent Administrator lead to the assessment that the MSG can successfully complete the quality assurance required according to Requirement 4.9 of the EITI standard on the basis of this system-based approach.

Type and scope of the work of the Independent Administrator

The work of the Independent Administrator consisted of investigative actions in accordance with the International Standard on Related Services (ISRS) 4400, Engagements to Perform Agreed-upon Procedures.

The investigative actions carried out by the Independent Administrator do not constitute a (final) audit or an audit review of the reported payment flows in accordance with professional standards for auditors recognised in Germany or internationally. Therefore, the Independent Administrator has not issued an overall judgement (neither with sufficient nor limited certainty) on the reported payment flows. The Independent Administrator has not carried out their own investigative actions to verify the accuracy, completeness and reliability of the payment data with regard to the data reports of the participating companies or the government agencies. Moreover, the investigative actions were not aimed at the detection of errors or infringements on the part of the participating companies or government agencies.

The activities of the Independent Administrator under the alternative reconciliation procedure were set out in a comprehensive work report for the 2023 reporting year.

Templates and information on data collection

Based on the MSG’s decisions on the D-EITI reporting process, the Independent Administrator has created a Word-based template for collecting the relevant data from the companies.

In order to provide companies with practical advice and assistance, a FAQ document (Frequently Asked Questions) was compiled in addition. In addition, the Federal Ministry for Economic Affairs and Energy (BMWE) provided an accompanying letter for the enquiry.

The template for data collection from companies also serves the MSG as a tool for communication with the participating companies to record the payment flows. Thus, at the request of the MSG and in line with previous years, additional enquiries were made regarding beneficial owners within the meaning of the Money Laundering Act and regarding the presence of so-called politically exposed persons (PEPs).

Managing tax secrecy

EITI reporting includes tax data, namely payment flows relating to corporate tax and trade tax, which are subject to tax secrecy in accordance with Sections 30 et seq. AO (German Taxation Regulation) (see comments under Tax secrecy). In the course of preparing the EITI report, the payment flows reported by the companies and received by government agencies were prepared and disclosed. This usage of tax-relevant data is only permissible if the taxpayer, i.e. the respective company, expressly agrees (Section 30 para. 4 No. 3 AO).

The data reporting by means of the enquiry form ensured that the consent of each individual company was obtained. This consent has been confirmed by all participating companies by the signatures of authorised persons.

Identification of companies

The Independent Administrator has carried out a comprehensive analysis to identify the relevant companies for the eighth D-EITI reporting. The analysis was based on the D&B Hoovers database. All the companies which are mainly active in the extractive industries in the areas of lignite, crude oil, natural gas, potash and salts as well as quarried natural resources were selected. This was based on the allocation of the companies to sub-sections 05 to 08 in accordance with Regulation 1893/2006/EC of December 2006 (see Selection of companies).

In the second step, the companies were selected according to the size criteria specified by the HGB for “large” companies.

The circle of these provisionally identified companies was manually expanded by the Independent Administrator to include corporate groups in which so-called group infection via “active” subsidiaries could be considered (for details see Selection of companies). The following aspects must be taken into account, unchanged from the previous D-EITI reporting:

- Companies which are primarily active in the storage of natural resources (e.g. construction and operation of cavern storage facilities for the storage of natural gas) are not considered, despite being assigned to sub-sections 05 to 08, since the extraction of natural resources is not the main focus here; the same applies to other services.

- All the companies in sub-section 07 (ore mining) initially included do not actively extract natural resources in Germany and were therefore not considered.

Due to the legal requirements (see Sections 341q et seq. HGB) and their interpretation, complete identification of all companies subject to reporting requirements for the current D-EITI reporting cannot be ensured. Nevertheless, the published payment reports for 2023 show that the companies determined according to the methodology used are broadly in line with the reporting companies.

It is evident that the selection criteria set by the MSG have achieved a high level of coverage for the lignite, crude oil, natural gas, potash and salt sectors (see 2023 payment flows). These natural resources are exclusively free-to-mine mineral resources. These sectors contain few large companies. On the other hand, the natural resources in the quarried natural resources sector are mainly produced by a large number of small to medium-sized companies.

According to evaluations by the Bundesverband Baustoffe – Steine und Erden e.V., there is a total of approx. 3,400 companies in the building materials, stone and earth industry in Germany in 2023. About 81% of these companies employ fewer than 50 people. These smaller units account for about 40% of the sales revenue of the building materials, stone and earth industry. The fragmentation of the sector is also due to the widely differing capital intensity of production; in particularly capital-intensive subsectors (e.g. cement production), larger medium-sized and large companies are significantly more represented than in the area of pure natural resource extraction. The size structure of the industry has changed little over the past decade.1

As a result, it can be assumed that a number of companies or corporate groups that do not meet the size criteria of the D-EITI reporting are already among the 25 largest providers in this sector. Coverage of the quarried natural resources sector therefore lags behind that of the other sectors, owing to the large number of small and medium-sized companies not covered.

Quality of data provided by companies

Companies in Germany are subject to comprehensive, legally-regulated

- accounting,

- disclosure, and

- auditing obligations.

The structure of the regulations depends on the size, legal form and activity of the company and must therefore be determined individually for each company. In principle, corporations and limited partnerships within the meaning of Section 264 a para. 1 HGB2 must draw up annual accounts with notes and, if necessary, a management report at the end of each financial year.3 The obligation to carry out an audit is regulated in particular in Section 316 et seq. HGB. There is a legal obligation to carry out audits for, among others, “medium-sized” or “large” corporations and certain limited liability partnerships. The size categories are determined according to Section 267 para. 2 and 3 HGB and are based on the criteria balance sheet total, turnover and average number of employees.

The statutory audit must include at least the annual accounts (balance sheet, profit and loss account and notes) as well as the management report and the accounting records. The auditor must determine whether the accounts are consistent with the underlying accounting principles and with any other legal basis such as the Articles of Association or the partnership agreement (compliance/regularity audit). Furthermore, it must be determined whether the respective financial statements together with the associated management report give a true and fair view of the company’s position, whereby it must also be examined whether the management report accurately presents the opportunities and risks of future development. The auditor summarises the results of the audit in a written audit report (see Section 322 HGB).

The annual accounts, management report and audit report (in the case of statutory audits) as well as other documents must be disclosed in the Company Register (Section 325 HGB). So they are generally available to the public at the internet address https://www.unternehmensregister.de/en. However, there are disclosure exemptions for certain size criteria.4

The shareholders of a subsidiary may waive the statutory audit and disclosure requirements for the annual accounts and management report of the subsidiary. This requires certain conditions (see Section 264 III HGB) to be met, including that the consolidated financial statements of the parent company are disclosed and that the parent company has agreed to assume responsibility for the obligations entered into by the subsidiary up to the reporting date. If the shareholders make use of all or part of the relief, these cases must, however, also be disclosed transparently via the Company Register.

In contrast to the annual accounts, the (group) payment reports are not subject to any statutory auditing obligation pursuant to Sections 341 q et seq. HGB. However, the statutory auditor

must report in the audit report if no (group) payment report has been prepared or disclosed despite the statutory obligation.

The management board or executives must ensure that the relevant financial statements are correct. To fulfil their due diligence obligations, they are usually supported by an internal audit department. The internal audit department provides independent and objective audit and advisory services. It supports the organisation in achieving its objectives by using a systematic and targeted approach to assess and improve the effectiveness of risk management, controls and management and monitoring processes. In Germany, there is no legal obligation to establish this process-independent control function, but it complies with the principles of good corporate governance (see German Corporate Governance Code). It is particularly common in large, complex or internationally active corporations.

In addition, many companies rely on compliance management systems to ensure compliance with legal requirements and internal policies. They include preventive measures, training or whistleblower channels to prevent or detect violations of laws or internal regulations. The establishment of a whistleblower system has been mandatory in Germany since 2023 for companies with 50 employees or more. The corresponding Whistleblower Protection Act (HinSchG) is the German implementation of the EU Whistleblower Directive.

Since the Financial Market Integrity Strengthening Act (FISG), listed companies also need to put in place an adequate and effective internal control system. An internal control system (ICS) consists of systematically designed technical and organisational measures and controls in the company to comply with guidelines and to prevent damage that can be caused by its own staff or malicious third parties. In particular, the accounting-related internal control system is geared to the accuracy and completeness of the financial statements.

Published accounts of the participating companies

The audited financial statements or consolidated financial statements are published on the websites of the participating companies or in the Company Register. Below is an overview with reference to the relevant documents.

Since it is technically not possible to link to individual enquiries in the Company Register, the following click instructions are included:

- Click on the linked website

- Enter the company name into the “Company name” search field

- If you select the “Extended search” option, you can narrow your search by stating specific criteria such as the registered office, subsidiary or desired publication period

- Select the corresponding documents according to the name in the table that subsequently appear

Identification of government agencies

Due to the federal structure of the administration in Germany, it is not possible to centrally record all the relevant government agencies that generate revenue from the extractive industry. They are therefore derived directly from the defined payment flows:

- Corporate tax: Competent tax offices at the registered office of the companies

- Trade tax: Municipalities in whose territory the relevant establishments are located

- Mine site and extraction royalties: Competent mining authorities of the federal state in which the licensed/approved field is located

- Lease payments and payments for infrastructure improvement: Government bodies at state or municipality level, depending on the type of payment

The basis for the presentation of government revenue is the corresponding data on payments by companies for the current reporting year.

Basis for risk identification and assessment

On the basis of publicly available sources of information, interviews with employees of the government agencies and the information provided by members of the MSG, it was assessed whether there were any indications that the following payment flows could be irregular in the 2023 reporting period:

- Mine site and extraction royalties

- Corporate tax and

- Trade tax

Details of this assessment process are described in more detail below.

The assessment is based on the processes and control mechanisms put in place by government agencies to ensure proper collection (debit) and settlement (payment) of the respective payment flows. The concept of “regularity” means, with regard to the EITI objectives,

- that adequate processes or procedures are in place at the level of the relevant government agency to ensure that payments are made in a timely manner and in accordance with the law,

- that processes and controls are in place to ensure full and timely clarification of any discrepancies between the debit position of government agencies and payments by companies,

- that adequate controls are in place at the level of higher government agencies; and

- that verification of the controls by independent audit offices is ensured.

The analysis of the processes and controls set up on the part of the government agencies therefore necessarily also takes into account the wider administrative environment of these government agencies and the relevant legal framework.5

In Germany, this system is based on a combination of legal bases (e.g. civil service law, budgetary law, criminal law, administrative regulations), the structure and organisation of the authorities (e.g. by means of rules of procedure, business allocation plans, establishment of segregation of duties, dual-control principle) and additional monitoring of processes and controls (e.g. by means of internal audit offices and other independent audit offices).

All these processes, procedures and controls are to be understood as an internal control system. An ICS supports the objective of a correct collection of the respective payments.

The definition of an internal control system is the result of various framework concepts. The concept of the Committee of Sponsoring Organisations of the Treadway Commission (COSO) has been widely disseminated internationally. Its basic principles are reflected, for example, in the Standards for Internal Control in the Federal Government of the United States Government

Accountability Office, which means that it can also be applied to government agencies. At the same time, this framework concept is, among other things, the methodological basis for the auditing standards applied in Germany by the Institut der Wirtschaftsprüfer in Deutschland e. V. (IDW) in statutory audits and voluntary audits.6

According to COSO, the components of an internal control system include the control environment, risk assessments, control activities, information & communication and monitoring of the internal control system. These components are applied to the relevant payment flows of corporate tax, trade tax and mine site and extraction royalties.

General information on the control environment with regard to the government agencies relevant for D-EITI

According to the Institute of German Auditors (IDW PS 982), the control environment is the framework within which regulations are introduced and applied. It is characterised by the basic attitudes, the awareness of the problem and the behaviour of the executives or management as well as by the role of the supervisory body (“tone at the top”). The clear design of the structural and process organisation should clearly define and separate responsibilities within the company. In addition, the essential regulations should be documented and made binding.

The control environment has a significant influence on the control awareness of the employees. A supportive environment can enhance the effectiveness of the internal control system. On the other hand, an unfavourable environment carries the risk that existing rules will only be formally respected or even ignored.

In the case of tax authorities (corporate tax), the control environment of the government agencies is characterised by a strictly hierarchical structure, which is in particular prescribed by the Financial Administration Act (FVG).7 The organisation of the mining authorities, on the other hand, is the responsibility of the respective federal state; the Federal Mining Act does not contain any detailed provisions in this regard.

Within the relevant government agencies, the respective organisational structure is clearly regulated by rules of procedure (e.g. the rules of procedure for the tax offices), business allocation plans, job descriptions and administrative instructions. The responsibilities of the respective job holders within the administrative processes result from the internal job descriptions or business allocation plans. The supervisory duties and powers of instruction of the respective superiors are derived from the rules of procedure and administrative instructions.

In addition, the control environment of the relevant government agencies is decisively shaped by German civil service law (Beamtenrecht)8 and parliamentary budgetary law and the associated control processes.

The civil service law is a separate area of law, which regulates the special rights and obligations of civil servants. The duty of neutrality in the exercise of their activities, the exclusion of the right to strike and the requirement of constitutional loyalty are contrasted with the right to lifelong employment with adequate remuneration and pension.

Breaches of duty by civil servants are subject to disciplinary law, a subset of civil service law. This governs how to proceed in the event of possible breaches of duty and what consequences are likely to result from proven guilt. Due to their special legal status, civil servants are obliged to behave with integrity. This includes, in particular, compliance with legal requirements and acting in accordance with the ethical principles of civil service law, including compliance with the law or the constitution. An important aspect of this obligation is the explicit release from the otherwise existing obligation of confidentiality under Section 37 para. 2 Sentence 1 No. 3 of the Civil Servants Status Act (BeamtStG), provided that a civil servant reports a fact-based suspicion of a corruption offence under Sections 331 to 337 of the Criminal Code to the competent supreme service authority.

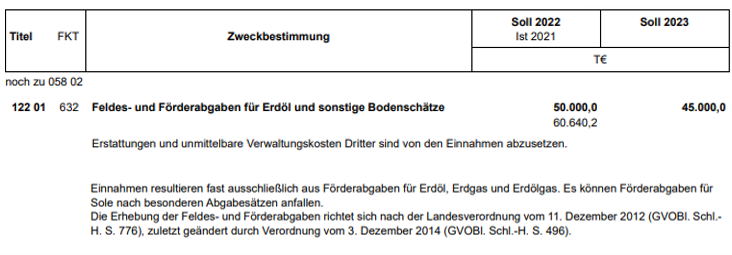

Furthermore, the relevant control environment is significantly shaped by the applicable budgetary law and the existing primacy of parliament at federal, state and local level. Parliament’s decision-making on Budgetary Law determines the budget in question and thus gains its democratic legitimacy. At the same time, Budgetary Law empowers the executive as well as obliges it to implement the budget in the respective financial year. Depending on the significance of the revenue for the budget, the payment flows relevant for D-EITI (corporate tax, trade tax, mine site and extraction royalties, lease payments, payments to infrastructure) are also shown separately in the budget planning or in Budgetary Law. Here is an example of the combined excerpt from the state budget of Schleswig-Holstein 2023:9

At the end of the fiscal year, the “budget account” is used to report on the financial results.

The budget account is a key instrument of public financial control. It documents how the appropriations provided for in the budget have actually been used. In this connection, planned and actual values are compared.

In addition to the above-mentioned regulations, Germany has a number of other regulations that are intended to ensure the integrity of the actions of public administrations. In the area of corruption prevention, especially the directive on corruption prevention in the federal administration should be mentioned, which contains essential measures of a prevention strategy such as

- the identification of work areas particularly at risk of corruption,

- the multiple-control principle; and

- the creation of a contact person

and a code of conduct for employees and guidelines for superiors and heads of authorities. Additional recommendations on corruption prevention in the federal administration serve to support the implementation of this directive. At the state level, there are also various legal regulations and administrative provisions to prevent illegal and unfair influences on administrative action (see the Corruption Prevention Act of 16 December 2004 as an example for NRW).

General information on the process risks

For a detailed assessment of the risks, the core processes of the assessment and survey are considered in more detail below.

Assessment process

The mine site and extraction royalties are based on a self-assessment by the respective companies. On the basis of the relevant legal regulations, the amount of the payment due is first determined by the companies themselves and communicated to the respective government agency.

The self-assessment procedure creates potential risks of error on the part of companies, for example:

- Writing or input errors when recording the data in the self-assessment,

- unintentional misinterpretation of relevant legal provisions,

- wilful disregard of legal requirements.

Accordingly, the relevant government agencies each have extensive auditing rights in order to ascertain whether the information prepared and provided is correct and complete.

There is no self-assessment in relation to income taxes (corporate and trade tax). The companies liable to pay tax have a statutory obligation to file income tax declarations, which must be submitted annually. Subsequently, the relevant and locally competent tax authority examines the information. After the income tax declarations submitted have been officially approved, income tax assessment notices and thus the amount to be paid are fixed and sent to the companies. Subsequently, tax returns may be reviewed in the course of tax audits.

The result of the assessment process forms the basis for the collection process, i.e. the actual payment flow. In this respect, the requirements of the EITI standard do not extend to the assessment process.

Collection process

Risks associated with the collection of payments must be distinguished from the risks in the assessment process. This process is called the collection process. A typical risk arises when employees take over tasks from both processes (assessment and collection process) and thus too much responsibility is bundled in one place.

The risk is addressed organisationally by a strict segregation of duties within the relevant government agency. Segregation of duties is defined by the division of responsibilities for specific, independent tasks of a business process between different persons or organisational units in order to minimise conflicts of interest, fraud and errors. In practice, therefore, the organisational separation between the assessment process and the collection process. The segregation of duties ensures that

- the employees responsible for the assessment have no access to the bank accounts of the government agency. The parties liable for payment transfer the specified amounts to these accounts, or these amounts are collected on these accounts.

- no one person handles the case in its entirety.

In the administrative organisation, special attention is also paid to ensuring that the dual-control principle is consistently adhered to in the administrative processes. Another aspect is the fact that companies can only meet their payment obligations by non-cash means. Payments may only be made by bank transfer; cash payments are not permitted.

Dealing with differences between the payment due and the payment received

Any discrepancies between the assessed payment due (debit position) and the actual payment received (actual receipt) will be clarified by the respective collection office.

If payments of corporate tax are too low, automatic reminders are sent in accordance with the statutory regulations or these payments are recovered by the enforcement office (as a special part of the collection office) within the framework of current legal regulations. If payments are too high, they are initially held safely (suspense account) by the collection office and offset against any possible other open positions owed by the taxpayer from other kinds of tax or other periods. If any difference remains after this, the taxpayer is reimbursed.

Comparable processes are established for the collection of mine site and extraction royalties. No automated reminders are sent to the payers because the number of companies that pay royalties is considerably smaller. Instead, reminders are handled by administrators on a case-by-case basis. For trade tax, the specific process design depends on the respective municipality, whereby the number of employees working in the processes varies with the size of the municipality. Basically, the responsibility for clarifying any discrepancies between payments due and payments received lies with the competent cash offices or the tax offices.

General information on the monitoring of processes and controls within government agencies

In the previous chapter, individual control measures in the assessment and collection process were described. These are, for example, the dual-control principle or the segregation of duties. In addition to these so-called process-integrated measures, an ICS also consists of process-independent monitoring measures.

The monitoring function is ensured, inter alia, by internal auditing units for both the corporate tax and the mine site and extraction royalties. The internal audit department performs an independent auditing function by investigating administrative actions for deviations and irregularities and making suggestions for their elimination and future avoidance. For trade tax, this monitoring function is implemented by the local audit processes. In addition, further monitoring for corporate and trade tax as well as mine site and extraction royalties is carried out by independent audit offices.

Corporate tax

As far as corporate tax is concerned, according to the information provided, the higher finance directorates or the state finance ministries carry out audits on an annual basis in the form of business audits. These audits relate to both the assessment and the collection area. Compliance with the regulations is checked on the basis of random checks.

In addition, a separate Internal Audit function is usually set up at the level of state finance ministries, which reports directly to the head of the authority. In the State of Hesse, for example, the work of the Internal Audit is based on the “Empfehlungen über Standards für Interne Revisionen in der Hessischen Landesverwaltung” (Recommendations on standards for Internal Audits in the Hesse State Administration). These standards form a uniform and cross-departmental working and legal basis. They are based on the auditing standards of the Deutsches Institut für Interne Revision e.V. (DIIR) and the “Empfehlungen des Bundesministeriums des Innern für Interne Revisionen” (Recommendations of the Federal Ministry of the Interior for Internal Audits).

Internal Audit prepares an audit report on its work, which is generally submitted to the management of the audited organisational unit for approval. The audited organisational unit receives a copy of this report. Internal Audit submits a written report on its activities to its management at least annually. This is without prejudice to audit-related reporting during the year.

The Federal Ministry of Finance may participate in external audits of the state tax authorities via the Federal Central Tax Office (Federal Tax Inspection) in accordance with Section 19 FVG. The Federal Ministry of Finance is hereby informed, inter alia, of tax developments which may be significant for legislative measures or administrative regulations.

Trade tax

For trade tax, the monitoring function is implemented by the local auditing. It is a supervisory body at municipal level that oversees the budgetary and financial management of cities and municipalities.10 It examines, inter alia, whether public funds have been used economically and appropriately. Local auditing works independently of the administration and reports directly to the municipal or city council. The aim is to ensure transparency and regularity in municipal budget implementation.

Local auditing is based on provisions of the respective municipal and state ordinances, for example the municipal code for the Free State of Bavaria (municipal code – GO). The tasks are carried out by different persons, agencies or bodies, depending on the relevant municipal regulations. In Bavaria, for example, they are taken over by the audit committee consisting of members of the municipal council. In municipalities with an audit office, the latter is also to be consulted as an expert.

Mine site and extraction royalties

The mine site and extraction royalties are generally monitored via the Internal Audit functions of the federal states. For example, in Lower Saxony, Internal Audit is responsible at the level of the Lower Saxony State Ministry of Finance for monitoring the procedures and controls within the Lower Saxony State Treasury. This is the payment processing body for the mine site and extraction royalties.11

Control activities relating to ongoing budget management are important at the state level. In Lower Saxony, for example, revenues in the budget execution system are allocated to the respective budget titles. This allows the responsible administrative unit to reconcile the planned revenue with the actual revenue. Depending on the importance of the mine site and extraction royalties for the respective budget, a comparison between planned and actual values over several financial years is possible in some cases. This creates transparency and enables the interested public to exercise a control function through political participation processes.

According to the survey conducted by the Independent Administrator, the mine site and extraction royalties are currently shown separately in the publicly accessible budgets of the states of Bavaria, Lower Saxony, North Rhine-Westphalia, Rhineland-Palatinate, Saarland, Saxony-Anhalt, Schleswig-Holstein and Thuringia.

Monitoring by independent audit offices

The various administrative units are also subject to auditing by independent auditing offices. These are municipal audit offices (e.g. Gemeindeprüfungsanstalt NRW), regional audit courts (Landesrechnungshöfe) or the Federal Audit Office (Bundesrechnungshof) (hereinafter referred to as audit offices).

The audit courts are independent supreme authorities of the federal government and the states. Their tasks, position and powers result from the Basic Law (Art. 114 GG) or the state constitutions.

Due to the federal state structure, Germany has independent audit courts at the federal and state levels to monitor budgetary management. The Federal Audit Office is solely responsible for federal finances.12 It has no supervisory rights or right to issue instructions to the regional audit courts.

Citizens, companies or organisations have the opportunity to address any information about possible maladministration directly to the Federal Audit Office. These so-called entries can be submitted by email or post. According to the Federal Audit Office, about one third of the submissions are answered directly, while the rest is forwarded to the competent audit departments and, if necessary, taken into account in audits.13

At the municipal level, the audit office consists of the supra-local audit. It is carried out by a state or association-affiliated audit office and constitutes an independent, supra-municipal, and state external audit. The audit is carried out by own municipal audit institutions (e.g. Gemeindeprüfungsanstalt NRW) or by the audit courts of the federal states or audit offices at district level. The audit serves, among other things, to promote the municipalities in economic and organisational matters by providing advice in a self-governing manner. In particular, suggestions for improvement are submitted to the auditees and comparative possibilities (including comparison of key figures) are used for this purpose.

The 20 state agencies with the highest trade tax payments for the 2023 reporting year are shown in the following overview with the relevant supra-local audit offices (audit institute/state audit court):

The following principles apply as a benchmark for the auditing of state and municipal budgetary and economic administration:

- the regularity of law enforcement and administrative action; and

- the economic efficiency and economical practices in budgetary and economic administration.

The principle of regularity includes, inter alia, the accounting correctness (proper and legal calculation, justification and accounting) of the individual invoice amounts. The respective audit court is solely responsible for the content, scope and frequency of the auditing procedures.

The audit results of the audit offices are made known to the bodies concerned in the form of audit reports. The audit court may, if it considers it necessary for specific reasons, communicate the results of the audit to bodies other than those audited. Selected audit results are nevertheless summarised in annual reports which are made available to the public, such as:

The current results of the audit offices show that their control function includes the (sub-)areas of the internal organisational and process organisation that are relevant for D-EITI. In this respect, the results of the audit offices appear to be fundamentally suitable and usable in terms of the risk-based alternative quality assurance procedure.

The German audit courts support the implementation of International Standards of Supreme Audit Institutions (ISSAI) developed within the framework of the International Organization of Supreme Audit Institutions (INTOSAI). The state audit courts are in international exchange and regularly discuss current standards and audit methods within the framework of the European Organization of Regional Audit Institutions (EURORAI). The maintenance of high audit standards at both national and state level can therefore be considered as given.

Information on the quality assurance process

Information on the quality assurance process for mine site and extraction royalties

The calculation, assessment and collection of the mine site and extraction royalties is based on the Federal Mining Act (BBergG) and the Extraction Royalties Ordinance of the respective federal states (see Mine site and extraction royalties) in conjunction with the relevant provisions of the German tax code (AO). Insofar as mining rights date back to the time before the current Federal Mining Act came into force in 1982 (“legacy rights”), no mine site and extraction royalties apply (see comments under “Authorisation of mining projects”).

In Germany, the State Office for Mining, Energy and Geology (LBEG), headquartered in Hanover, is responsible for the vast majority of mine site and extraction royalties. The LBEG is supervised by the Lower Saxony Ministry of Economic Affairs, Labour, Transport and Digitalization.14

Based on the control environment presented and the existing processes and controls, there was no evidence of an increased risk with regard to the regularity of the settlement of the payment flow of the mine site and extraction royalties. As a result, within the scope of the alternative quality assurance procedure, there will be a plausibility check of the reported payments of the companies.

Based on the analyses conducted by the Independent Administrator and publicly available information, the results of the amounts of mine site and extraction royalties for the 2023 reporting year appear to be comprehensible and plausible in terms of content.

Information on the quality assurance process for corporate tax payments

The reported data on the corporate tax payment flow are presented below.

Compared to the previous year, no corporate tax payments by Dyckerhoff GmbH were shown. This is because the main activity is the production and distribution of cement and not the extraction of the natural resource limestone.

Based on the control environment presented and the existing processes and controls, there was no evidence of an increased risk with regard to the regularity of the settlement of the payment flow of the corporate tax. As a result, within the scope of the alternative quality assurance procedure, there will be a plausibility check of the reported payments of the companies.

Based on the analyses conducted by the Independent Administrator and publicly available information, the results of the amounts of corporate tax for the 2023 reporting year appear to be comprehensible and plausible in terms of content.

Information on the quality assurance process for trade tax payments

The upstream process for assessing trade tax is primarily carried out by the tax offices, which draw up a trade tax assessment notice as a basic notice. Based thereon, the municipalities calculate the specific trade tax liability by applying their individual tax factor. The amount of the tax factor therefore varies according to the municipality and is decided in the respective cities and municipalities by parliamentary procedure.

For the fifth D-EITI report, the trade tax collection process was further analysed by means of a questionnaire developed by the Independent Administrator. This questionnaire was sent to the 20 municipalities that received the highest trade tax payments from the participating companies for the 2020 reporting year. The answers resulting from the questionnaires provided the MSG with an insight into the processes and controls set up by municipalities of various sizes to ensure the trade tax is collected correctly.

The following lists the 20 municipalities with the highest trade tax payments with the corresponding companies for the current 2023 reporting period.

In line with previous years, the group of municipalities with the largest trade tax payments is dominated by companies from the crude oil and natural gas sector. Overall, the group of municipalities with the highest trade tax receipts is subject to only minor changes over the last reporting years, so that the findings and results from the survey for the 2020 reporting year were also used for the current reporting period. There are no findings to the contrary, for example from the findings of the MSG.

The main findings of this survey and system analysis can be summarised as follows:

- The recording of the payments and the reconciliation with the existing receivables from the companies is mostly automated. In the event of discrepancies between payment and receivables or incomplete or incorrect information, manual follow-up is required. The number of employees working in the process varies significantly between municipalities depending on the size of the respective municipality. The number of employees in the cash office is always higher than the number of employees responsible for exemption from trade tax. The close integration with the tax offices in the assessment process has a direct impact on the processes in the municipalities – especially through the basic notices of the tax offices, on which the municipalities base their further steps.

- The separation of the two administrative steps of assessment and collection in terms of personnel is ensured; the basic principle of separation of functions is thus respected regardless of the size of the municipality. Unclear payments are generally handled by the cash office. In individual cases, consultation with the authority responsible for issuing the trade tax assessment notice is necessary.

- In the context of taxation, equity measures may exceptionally be applied. This means both the deferral of payments and the definitive waiver of trade tax claims, in compliance with the respective provisions on these equity measures. In principle, this is decided within the municipality’s administration; only in individual cases does the municipality follow the corresponding decisions of the tax administration for corporate tax. The respective decision-making processes take place outside the cash office and, depending on the importance of the respective equity measure for the respective budget, require the involvement of higher-level decision-makers up to the mayor or the main or administrative committee (a permanent, representative committee of the municipal parliament or municipal council).

- The quality of the organisational processes and structures or controls set up is comparable to the processes and controls of the payment flows of corporate tax and mine site and extraction royalties. Nevertheless, the organisation and content of payment processes in the municipalities can differ in detail, especially depending on their size.

The following overview shows how many municipalities received trade tax payments from each participating company in 2023.

Based on the control environment presented and the existing processes and controls, there was no evidence of an increased risk with regard to the regularity of the settlement of the payment flow of the trade tax. As a result, within the scope of the alternative quality assurance procedure, there will be a plausibility check of the reported payments of the companies.

Based on the analyses conducted by the Independent Administrator and publicly available information, the results of the amounts of trade tax for the 2023 reporting year appear to be comprehensible and plausible in terms of content.

Insight into the Transparency Register and PEP evaluation

In the context of the 2023 EITI reporting, the Independent Administrator inspected the Transparency Register. It was verified whether the participating companies had an entry in the Transparency Register and whether this entry was reconcilable on the basis of the available information. The Independent Administrator received a Transparency Register extract for all participating companies. In this context, the Independent Administrator reports that entries in the transparency register were available for all of these companies and that these entries are considered plausible.

Insofar as natural persons have been identified as beneficial owners in the Transparency Register, the Independent Administrator has decided whether they are “politically exposed persons” (PEP). The basis for the definition of a PEP was the country-specific categories published by the EU.15 On the basis of this investigative act, it was found that there was one PEP among the participating companies. This is a legal representative of a participating company who was part of the board of a state-owned company in their previous employment. This employment relationship was less than 12 months prior to the reporting year.

Following the judgement of the European Court of Justice (ECJ) of 22 November 2022 in joined cases C-37/20 and C-601/2016, the Transparency Register has made public access to any interested party conditional on the existence of a legitimate interest, a condition which remains in force at the time of publication of this report. The Transparency Register granted the Independent Administrator access on the basis of a legitimate interest so that the information could be obtained and analysed for the participating companies.

Proportion of women in the participating companies

An analysis of publicly available data on the participation of women in top management, the two highest levels of management and the supervisory board of companies participating in D-EITI reporting was carried out. The analysis was based on the following sources:

- Annual and Consolidated Financial Statements and Annual Reports, available at unternehmensregister.de,

- Extracts from the Commercial Register or list of supervisory board members, available at handelsregister.de,

- Publicly available information on the websites of the participating companies.

The amount of information available on the participation of women in management, the two highest levels of management and the supervisory board differs fundamentally between the participating companies. These differences arise from the respective different legal disclosure requirements, which depend on the size of the company, its legal form, its listing on the stock exchange and whether the company is subject to codetermination.

If one of the participating companies did not publish individual financial statements, the information from the consolidated financial statements was used instead. The determination of the participation rates in the company management and the Supervisory Board took place exclusively as of the reference date 31 December 2023. Changes during the year – for example, through changes of members – were not proportionally taken into account.